3 practical things to remember in times of economic uncertainty

26/05/22

Over the last few months, you can’t have missed the tough economic headlines. You’ve also likely seen the impact of the global economy on your own finances.

Whether it’s the rise in the energy price cap and the rate of National Insurance contributions (NICs), the increasing cost of goods and services, or the impact of stock market volatility on your pensions or investments, it’s been a tricky 2022 so far.

It’s natural to feel nervous or worried when national or global events have a direct influence on your wealth.

2022 has seen a conflation of events, from global supply chain issues to the Russian invasion of Ukraine. Throw in inflation hitting a 40-year high, rising interest rates, and the continuing effect of both Brexit and Covid, and it’s easy to see why things might have been a little uncertain.

Read on to find out more about how markets have fared so far in 2022, and three practical things to remember during difficult periods.

Markets have endured a volatile start to 2022

With the exception of the UK FTSE All-Share index, global stock markets have mostly seen a downturn at the start of 2022.

The table below shows the performance of a range of regional indices between January and the end of April 2022.

Source: JP Morgan. Figures from FTSE, MSCI, Refinitiv Datastream, Standard & Poor’s, TOPIX, J.P. Morgan Asset Management. All indices are total return in local currency, except for MSCI Asia ex-Japan and MSCI EM, which are in US dollars. Past performance is not a reliable indicator of current and future results. Data as of 30 April 2022.

April was particularly brutal in US markets. CNBC report that the Nasdaq fell about 13.3% in April, its worst monthly performance since October 2008 during the global financial crisis.

The S&P 500 lost 8.8%, its worst month since March 2020 at the onset of the Covid pandemic, while the Dow Jones fell by 4.9%.

Of course, different regions have reacted differently to the current issues.

This is one reason it’s important to hold a diversified portfolio, as falls in one region can be offset by rises elsewhere. While US markets may have fallen, the FTSE 100 is broadly at the same level it started 2022, helping to balance the performance of your portfolio.

If you’re concerned, here are three things to always remember during uncertain times. We hope they may help you to manage any anxiety you have about your finances.

1. Cash is not always king

In times of volatility, it can be tempting to exit the stock market altogether and move your money into cash savings. Keeping your money in the bank or building society might reassure you that it won’t “lose” value.

However, there are two important points to bear in mind.

Firstly, if you sell your investments during a downturn, you are effectively turning a paper loss into an actual loss.

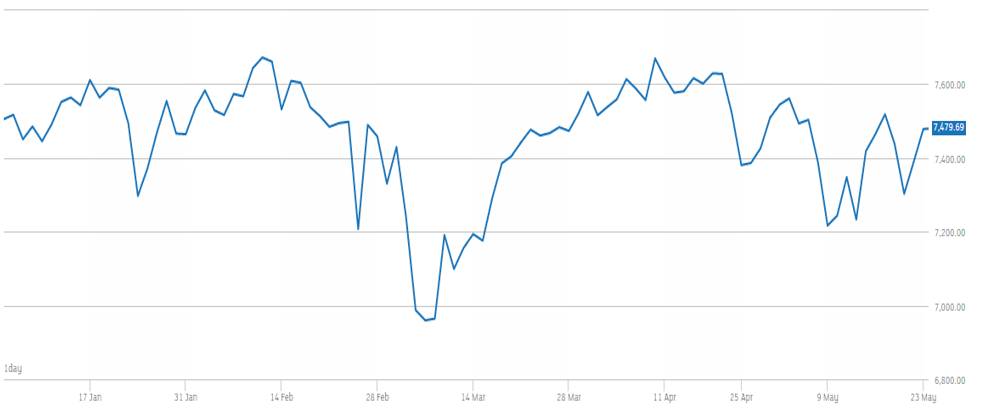

Here’s the performance of the FTSE 100 from the start of January to 23 May 2022.

Source: London Stock Exchange

If you’d decided to sell and exit the market at the start of March, you’d have missed out on the subsequent growth in April and May.

Secondly, while you may not “lose” money by keeping your wealth in cash savings, you are almost certainly eroding its value in real terms.

The latest Office for National Statistics (ONS) data shows UK inflation reached 9% in April. Compare this to the highest interest rate you can receive on easy-access cash savings in May 2022 which, according to analysts Moneyfacts, is just 1.25%.

- If you save £100,000 at 1.25% you’ll earn £1,250 interest, so your cash in a year will be worth £101,250.

- If inflation remains at 9%, £100,000 worth of goods and services now will cost £109,000 in 12 months’ time.

- In real terms, keeping your wealth in cash has hugely eroded its buying power.

While it’s important to keep some money in cash – we can work with you to establish exactly how much – keeping too much in cash can slow your progress towards your long-term goals.

2. If your goals haven’t changed, neither should your plan

The key to successful financial planning is about establishing your goals and devising a plan that can help you to reach them. These might include protecting your loved ones, retiring early, or helping your children through education or onto the property ladder.

When we devise a plan, we factor in all sorts of unknown variables. These will include periods of investment uncertainty, inflation and, of course, changes to your own circumstances.

Remember: your plan already assumes that there will be tricky periods in the markets!

If your long-term goals haven’t changed since the start of the year, it’s unlikely that your plan will need to change either.

Your goals might be 10, 20 or even 30 years in the future, so the performance of the stock market in May 2022 is, in the overall scheme of things, not going to make an enormous difference to you meeting your goals.

Instead, have faith in the process, and in the plan. In the long term – and that’s what you’re likely to be investing for – markets tend to offer positive returns.

As Paul Samuelson said: “Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.”

3. Investing after a downturn could provide rewards

Warren Buffett, often seen as one of the world’s leading investment gurus, has a useful quote for periods of economic uncertainty: “Be fearful when others are greedy, and greedy when others are fearful.”

What he means is that investing in a falling market can offer benefits when markets recover which, history tells us, they almost always do.

It’s impossible to guess when the bottom of the market is, even for experienced fund managers.

However, had you decided to take a contrarian view and invested after the significant downturn in the markets when the first lockdowns were mandated in March 2020, you’d have seen positive growth on your investments since that time.

Sometimes, looking at a period of uncertainty as a potential opportunity can change your mindset. Of course, you must remember that past performance is not a reliable indicator of future performance and that the value of your investment can go down as well as up and you may not get back the full amount you invested.

We’re here to help

Benjamin Graham once said: “The investor’s chief problem – even his worst enemy – is likely to be himself.”

When times are uncertain it’s easy to act on emotion. Your behavioural biases kick in, and you might make knee-jerk decisions that can impact your long-term goals.

That’s why we are here. We can chat through the current situation with you, review your plans and your goals, and give you the reassurance that you’re on course. And, if you’re not on track, we can take steps to ensure your goals remain attainable.

If you would like to chat to us about the current uncertainty, or you’d like to review your financial plan, please get in touch.

Please note

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.